The next unbundling

Asserting that AI will fundamentally change the future is obvious, but saying precisely how it will change the future is more fraught.

To be sure, we have been pulling on a number of strings to disentangle the problem for our business but until recently we have held back on making determinations on exactly what this will look like. This is our first thrust to define how we think things will unfold in the niches where we operate.

It's hard to overstate the leverage in productivity to which AI will give rise, especially among the expert-class. For one, experts are able to discern more readily when models are hallucinating or just plain wrong than non-experts, but more interestingly something like autonomous agents are able to distill and then replicate an expert ad-infinitum. To put a finer point on it; AI removes the bottleneck that previously made professional services firms difficult to grow.

This might result in much more scalable professional service firms where top individual contributors are able to extend themselves to a position where they might be able to serve multiple companies (or clients) more effectively and cheaply than companies hiring and building those teams internally.

The practical example that brought this home for me was seeing a start-up team running an attention agency managing social-media pages for clients for c. GBP 2,000 - 4,000 per month, seemingly with much better results than their clients would have achieved owning this internally and at probably 5-7x the scale of an IC within a single organisation.

This poses the question whether firms are better to unbundle these functions or maintain the status quo?

Two classical models of economics are relevant for this discussion -

Comparative advantage: David Ricardo’s model for comparative advantage is no less relevant than before. If the diffusion of AI leads to greater competition among organisations AND it becomes easier for these organisations to narrow their areas of focus to only the capabilities that provide a source of differentiation for them (which they probably will have to do regardless given increased competition), they will unbundle non-core activities to the extent possible.

Transaction costs: Ronald Coase’s ‘Coaseian Floor’ states that firms will keep growing until the cost to organise a marginal transaction outside the firm is less than or equal to the same transaction inside the firm. If you believe AI makes it easier to discern expert quality, standardise pricing and for firms manage and police output, transaction costs are likely to decrease materially.

Assuming the above is true, the question in the nearterm is whether the unbundling is either from (i) employees to AI or (ii) from employees to specialists who are really good at using AI? In the long-term, the benefits and economics will most likely accrue to AI / systems in most non-specialised and repetitive workloads. In regulated, creative or non-repetitive industries and workloads, experts are probably likely to be relevant for some time to come.

All else being equal my view would be the latter in a like-for-like competition, if for no other reason that (i) it will probably be some time before AI can operate without any human involvement at all, and (ii) an expert who knows how to effectively use AI tools or tweak them is likely to outperform a model operating alone.

What is the current reality?

Looking across a sample of about 10 firms, my best baseline estimate is that the marginal expert who is proficient in the requisite AI tools would be about 6x as productive as an individual employee within a firm. Assuming we roll forward the general ‘contractor premium’ of c. 75% and add another 25% - 30% to account for the tokens and compute, an unbundled expert should be able to deliver a premium service at c. 33% of the cost of an employee at full capacity. Building this up to the firm level (adjusting for overhead, SG&A etc.), our best estimate is that an unbundled expert should be able to deliver above spec for c. 55% of the cost of an employee.

I suspect as models improve, Q&A gets better and the broader set of integrations and connectors for AI is built out, the relative savings on a like-for-like basis would approximate 60 - 70%, i.e. an unbundled expert would deliver a better service for 30-40% of the cost of an internal function.

What is the opportunity?

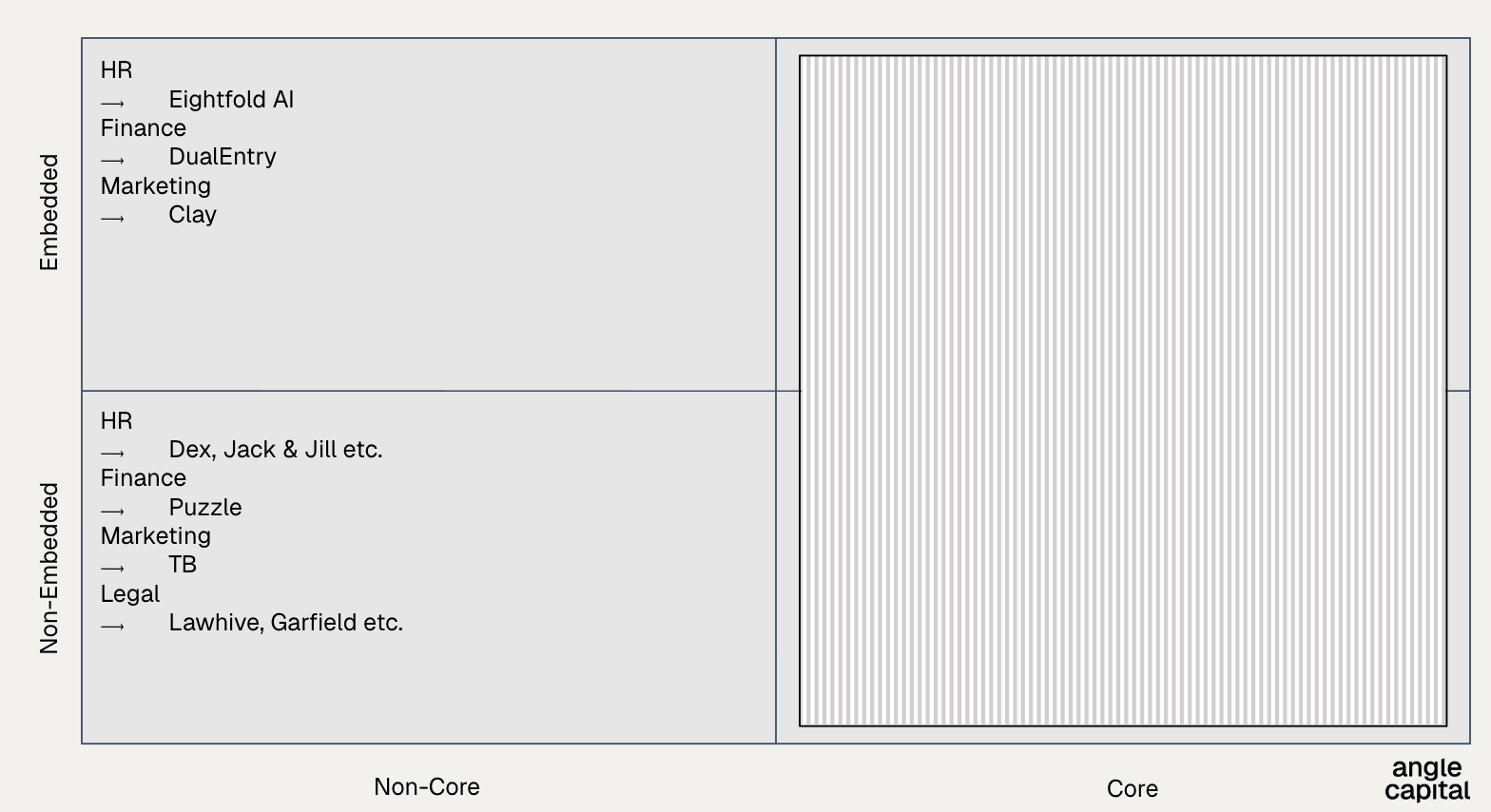

The opportunity cuts into two-planes; (i) core vs non-core functions (generally non-core being unbundled) and (ii) embedded vs. non-embedded systems. Non-core functions generally look like HR, finance, (in some cases) marketing and PR, and back-office IT. Embedded systems are deeply integrated systems which look and feel like enterprise software businesses whereas non-embedded systems approximate professional service firms.

Embedded systems would be relatively more capital intensive and have naturally higher CAC, but will be sticky and hard to replace once embedded. Non-embedded systems should be relatively capital light and quick to generate cash, though defensibility would need to be sought outside of any potential integration value that would come from a pureplay software model. Below are a few modern examples in each of the planes.

Building durable value?

Growing an enduring business in an embedded vs. non-embedded category will be different. We see the primary differences as follows -

Embedded:

- Core challenge: Long, complex sales cycles.

- ‘Must-nail’: High initial ACVs in order to be able to fund GTM and a strong, low friction initial wedge.

- Defensibility: As mentioned earlier, our view is that embedded systems will resemble software firms more than professional service firms, which is to say that defensibility will arise from the extent of their integration and adoption within the environment of their clients, which will come down to product and sales (including customer success). Though sales is likely to be less idiosyncratic, product differentiation will be driven by design and enduring sources of proprietary data.

Non-embedded:

- Core challenge: Non recurring revenue with higher cyclicality.

- ‘Must-nail’: Given their core challenges, these firms need to have very low CAC and focus on a broad surface in which to service clients to counteract the lower revenue recurrence.

- Defensibility: AI-native service firms differentiate on service, price and brand. (i) Service quality is a function of the expertise of the team and the data-set on which the AI is developed, (ii) price is a function of economies of scale which come down to the quality of the system on the one hand and the commercial usage of a system on the other, and (iii) given that it's easier than ever before to start a company, spin-out a team or develop the marginal ‘ai-solution’, the proliferation of new firms will likely be immense and brand therefore critical to help users discern.

Maybe this is a natural eudaemonic filtering process we are seeing unfold in real time; (1) the specialists who enjoy the craft embrace the tools and reap the benefits, (2) the rest are unbundled to find their bliss elsewhere, (3) David Ricardo strikes again (4) evolution marches the economy forward.

Philosophy aside, if you are building a recurring non-embedded next generation AI services firm, a non-obvious and capital light embedded system or have thoughtful disagreements which might help improve our thesis, get in touch at Nic@anglecap.com or Mart@anglecap.com.