If the music continues to slow

My sense is that it will only get harder for the median start-up to raise capital in the US, EU and UK. Founders not building the marginal ‘hot-AI-company’ need to be extremely thoughtful about managing runway, burn and fundraising dynamics; they shouldn't assume investors will be waiting +18 months after raising their last round… Below are some factors driving a more difficult fundraising climate in our view, which doesn’t show any signs of abating.

%20(1).png)

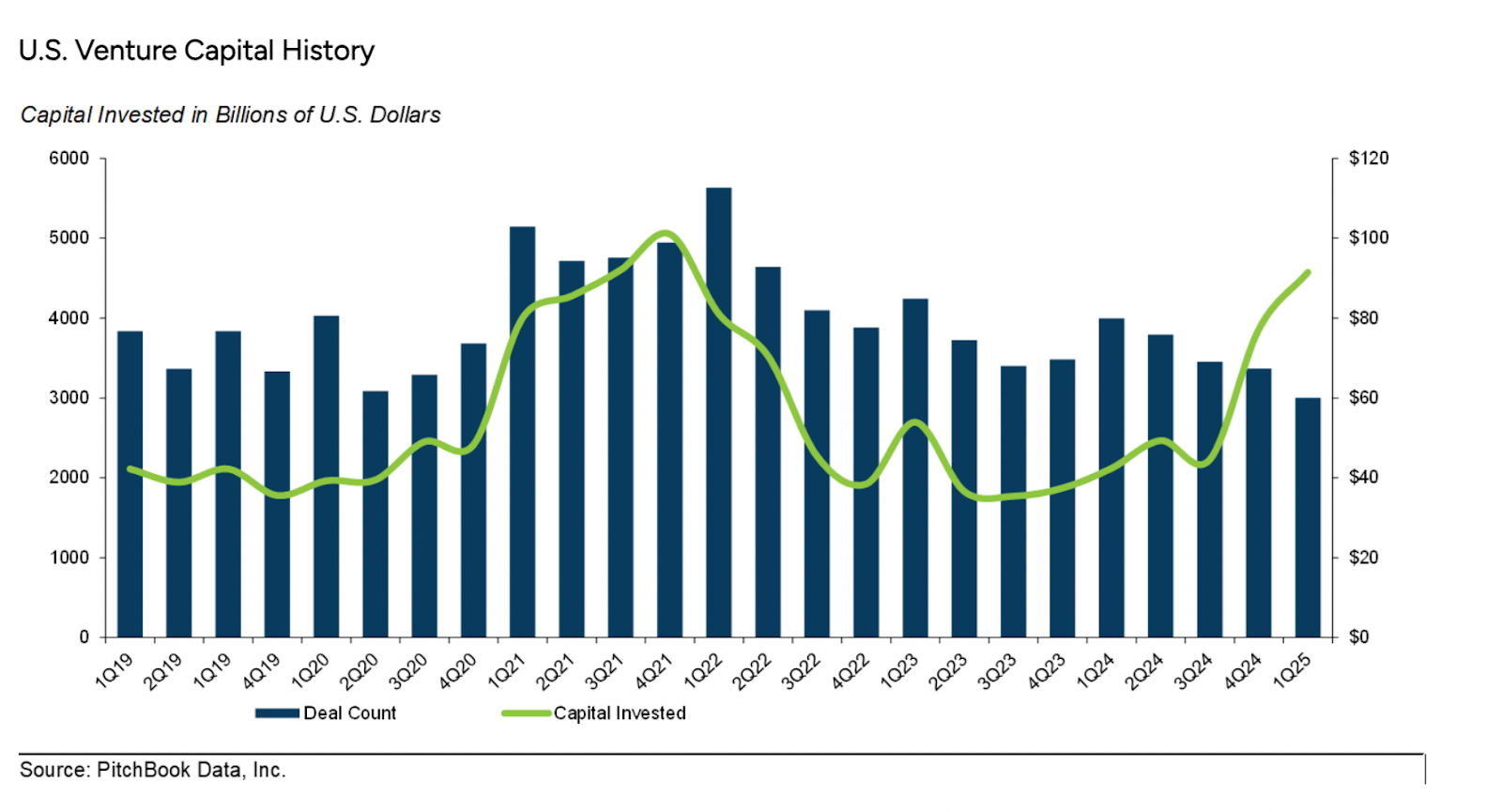

Fewer companies are raising capital in a more concentrated way: Contrary to what many of the headlines and public market performance may suggest, fewer companies are getting funded (below 2019 deal count) and capital is getting concentrated in fewer companies, which is to say it is getting harder for the median startup to raise capital. (Of the c. USD 100bn in funding raised during Q1, OpenAi and Databricks accounted for roughly 50%, which if you strip out, gets funding levels back to Q1 ‘19.)

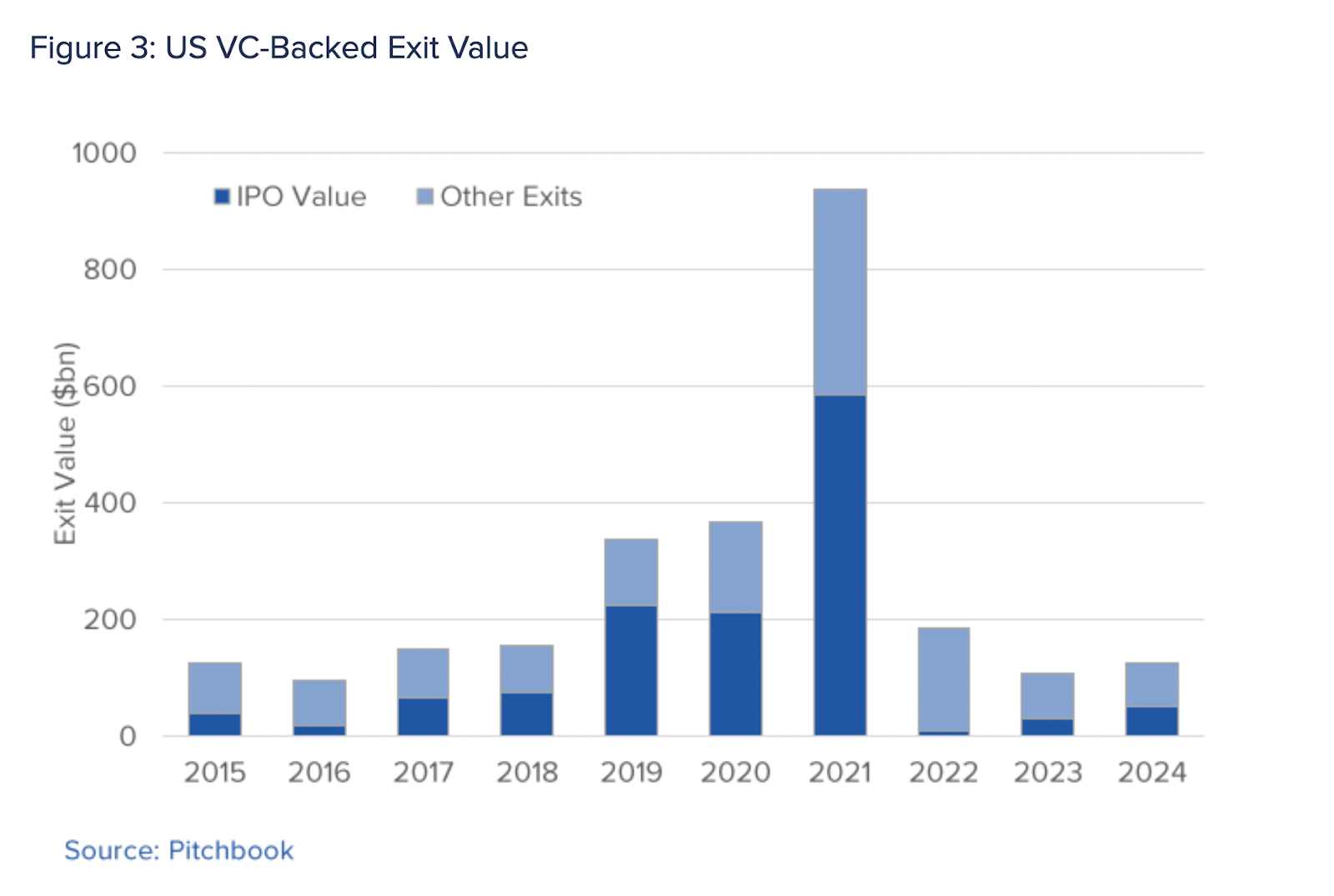

LPs are investing less in the asset class: Total dollars available for VCs will be less in the future: (i) LPs are rebalancing from having been overinvested for the last c. 10 years; (ii) returns for the asset class is looking increasingly poor given heightened competition and; (iii) limited DPI, which doesn’t seem to show signs of improving as companies are staying private for longer.

Fundraising for funds is back to 2019 levels -

DPI is at c. 2015 levels -

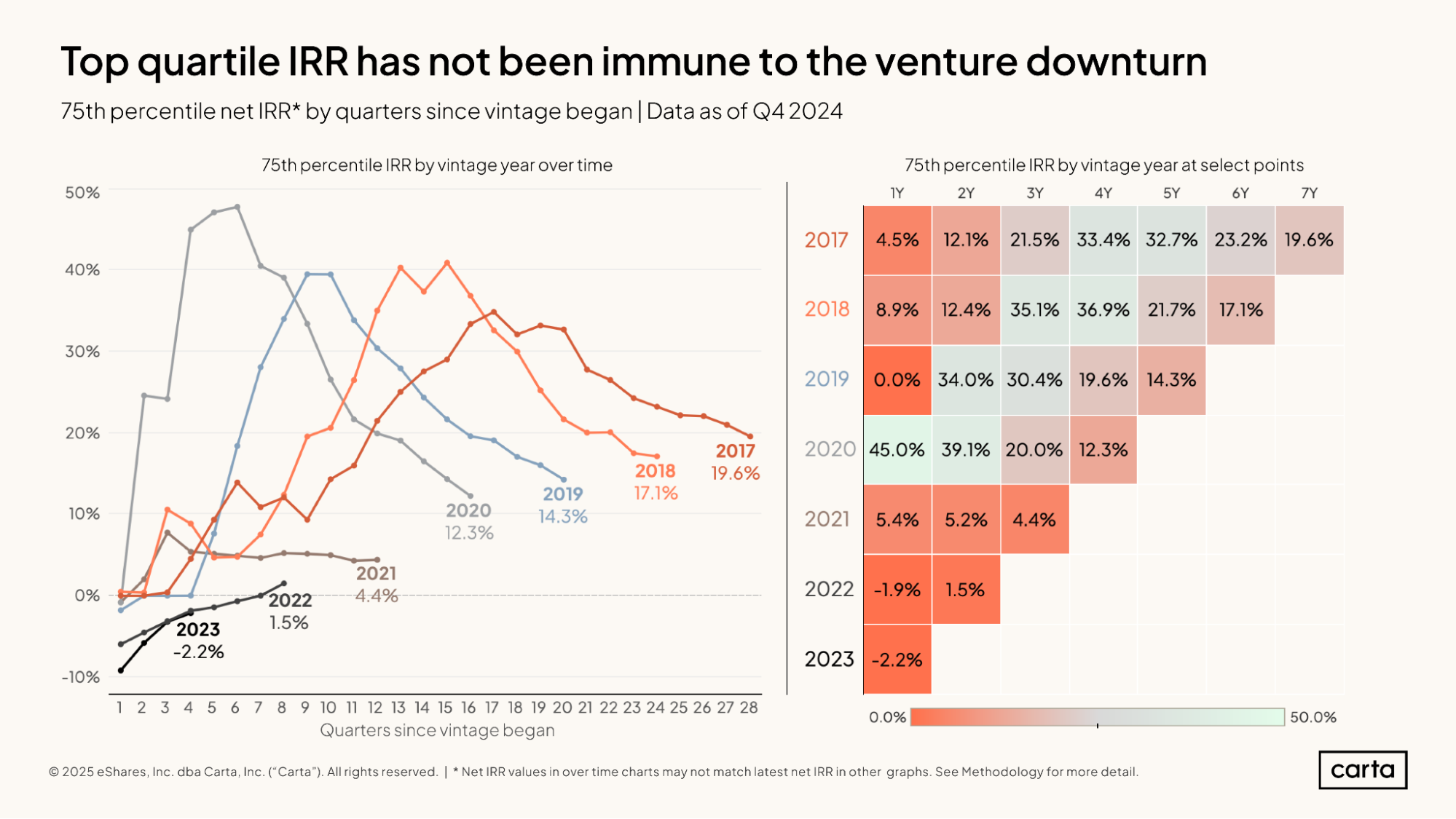

Returns are getting worse -

Experimentation will fade among enterprises: As AI becomes scaled within organisations, enterprises will naturally experiment less which will make it harder for multiple companies in the same category to win budget for trials. The downstream implications of more turbulent revenue scaling for new projects will cause investors to pull back…

‘Risk-off’ happens faster than you think: We are certainly not calling any ‘bubbles’ in private markets, though things certainly seem overheated. During periods of stress, capital decreases materially; following corrections such as ‘00 - ‘02, ‘08 - ‘09 and ‘16 - ‘17, it's not uncommon for funding to fall by 40 - 80% peak-to-through within a 12 month window..